TL;DR:

- High-performing investors prioritize systems and buffers over sheer effort to maintain decision-making quality and longevity. They build disciplined habits around financial buffers, vitality routines, and continuous learning to sustain modular performance across decades. Integrated, systemic approaches grounded in consistency and non-negotiable minimums drive sustained success beyond isolated optimization.

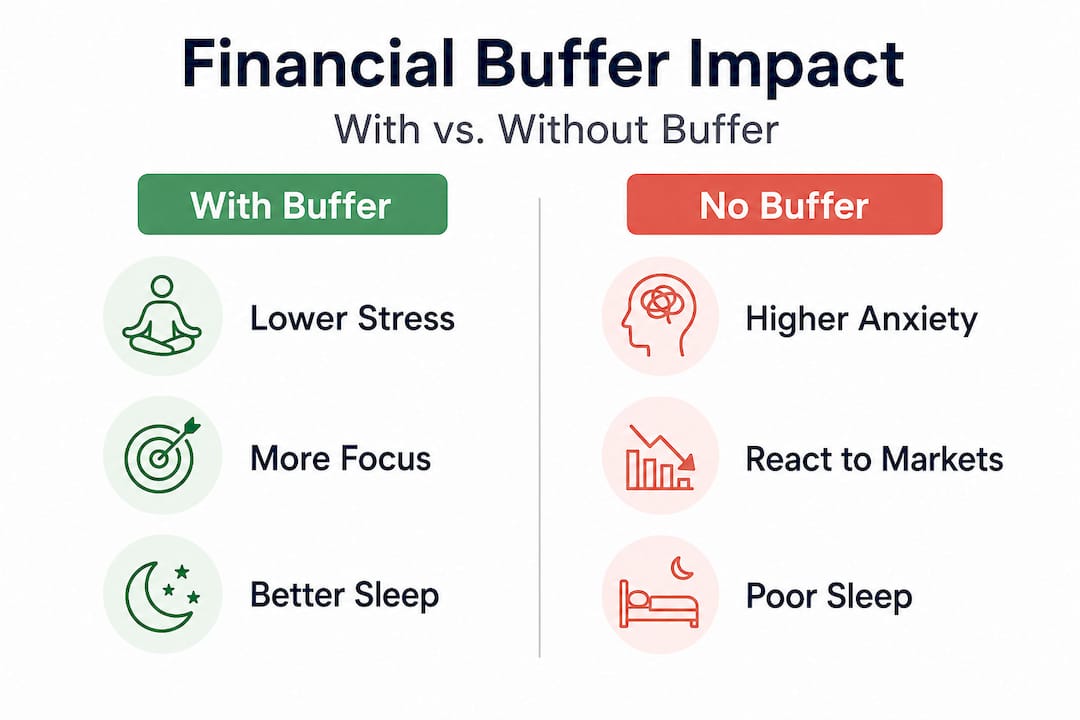

Most high-performing investors don't burn out from too much work. They burn out from the wrong kind of systems — or no systems at all. The real threat isn't a brutal deal cycle or a volatile quarter. It's the slow erosion that happens when financial uncertainty, poor recovery habits, and absent growth routines pile up silently in the background. Emergency savings alone correlate to a 21% higher level of financial well-being, which tells you something important: the structural choices you make around money and health are not separate from performance. They are performance.

Table of Contents

- What defines the investor lifestyle?

- Core systems: The financial foundation for investor well-being

- Energy, health, and high-agency performance routines

- Integrating growth: Personal development in the investor lifestyle

- Why most investor lifestyle advice fails (and what actually works)

- Take your investor lifestyle to the next level

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Buffer stress with systems | Emergency funds and automation lower daily anxiety and boost long-term decision quality. |

| Structure routine for vitality | Consistent health habits and social recharge blocks are the backbone of high performance. |

| Growth is scheduled | Personal and professional development only becomes routine when it’s intentionally built into your calendar. |

| Integrate financial and physical | Separating money health from body health is a mistake—true long-term results come from aligning both. |

What defines the investor lifestyle?

The phrase "investor lifestyle" gets thrown around carelessly. In the popular imagination, it means expensive watches, early mornings, and an obsessive relationship with portfolio returns. That picture isn't wrong, exactly. But it's incomplete in ways that cost people their edge over time.

A genuine investor lifestyle, at the highest level, is about sustained output over decades. That means vitality is not a luxury layer you add when things slow down. It's a core performance asset. The men who operate at the top of their game into their 50s and 60s didn't get there by grinding harder than everyone else. They built systems: financial buffers, movement habits, cognitive recovery protocols, and learning routines that compound just like capital does.

Consider the structural challenge. Markets move unpredictably. Deal flow is non-linear. The cognitive load of managing complex portfolios, relationships, and strategic decisions is significant. Without buffers — both financial and biological — that load creates what researchers call "background stress," a constant low-level drain that degrades decision-making, shortens recovery windows, and narrows creative thinking. You don't notice it day to day. You notice it five years later when your judgment feels slower and your energy ceiling has dropped.

The investor lifestyle at its best is not about maximizing work hours. It's about maximizing the quality of your decisions, your energy, and your longevity in the game. Everything else follows from that.

This is why vitality optimization for men in the 40 to 65 age range is not about fitness vanity. It's about preserving the biological substrate of high-level thinking and judgment. Market volatility erodes performance unless buffered by stable systems. That applies to your balance sheet and your body simultaneously. Automated savings and financial buffers reduce emotional load during volatile periods, clearing cognitive bandwidth for the decisions that actually matter. A longevity lifestyle integrates both sides of that equation.

The real pillars of the investor lifestyle:

- Sustainable output over decades, not sprints

- Financial buffers that reduce anxiety and cognitive noise

- Vitality systems that support peak judgment and energy

- Growth habits that keep strategic thinking sharp and adaptive

Core systems: The financial foundation for investor well-being

Most conversations about investor performance focus on alpha generation, portfolio construction, and market timing. Few focus on the foundational financial habits that reduce the chronic stress load that undercuts all of it. That's a gap worth closing.

The data is straightforward. Having at least $2,000 in emergency savings is associated with a 21% higher level of financial well-being compared to having none. For a high-net-worth investor, $2,000 sounds trivially small. But the principle scales. It's about liquidity that is ring-fenced from investment capital, available immediately, and not subject to the psychological weight of "should I sell something?" during an unexpected event. That available buffer directly reduces the activation of stress responses during volatility.

Automation compounds this effect. Automated savings and automated bill payment remove hundreds of small cognitive decisions from your week. Decision fatigue is a real and measurable phenomenon: the more trivial choices you make, the worse your judgment gets on important ones. Investors who automate the routine and reserve their cognitive firepower for strategic thinking consistently demonstrate sharper execution.

Comparison: investors with and without financial buffers

| Factor | With strong financial buffers | Without financial buffers |

|---|---|---|

| Stress response during volatility | Reduced, manageable | Elevated, reactive |

| Decision quality under pressure | Higher, more deliberate | Degraded, impulsive |

| Recovery time after setbacks | Faster | Slower |

| Long-term strategic clarity | Clearer | Clouded by short-term anxiety |

| Overall financial well-being score | Significantly higher | Significantly lower |

The contrast is not theoretical. Investors without adequate liquidity buffers often make reactive selling decisions at market lows, not because they lack knowledge, but because the psychological pressure of illiquidity overrides rational judgment. This is peak executive performance seen from its underside: smart people making poor decisions because their foundation is structurally unstable.

Core financial system habits for investor well-being:

- Maintain a dedicated liquidity buffer separate from investment capital

- Automate savings contributions to remove willpower from the equation

- Review and adjust budget allocations quarterly, not reactively

- Eliminate recurring financial decisions wherever automation is possible

- Build a personal financial dashboard that gives you clarity in under five minutes per week

Pro Tip: Treat your personal liquidity buffer the way you treat portfolio risk management. Define a minimum threshold, make it non-negotiable, and review it on a fixed schedule rather than reactively.

Energy, health, and high-agency performance routines

If financial systems are the foundation, physical and cognitive energy are the operating system. Without them, even the best strategy fails at execution.

The evidence from people who operate at the intersection of high finance and long-term vitality is clear and consistent. A longevity investor's daily routine typically includes structured practices: intermittent fasting, approximately one hour of daily physical activity, a 10,000-steps-per-day baseline, deliberate attention to mental health, and weekly blocks dedicated to social connection and learning. These are not aspirational habits. They are operational ones.

Intermittent fasting, specifically time-restricted eating windows of 16 to 18 hours, reduces inflammation markers, improves insulin sensitivity, and stabilizes energy across the day. For investors whose cognitive performance must be sharp from early morning calls to late-evening negotiations, stable energy without dramatic post-meal crashes is a competitive advantage. The men who skip this are essentially accepting an unnecessary performance handicap.

Physical activity at roughly one hour per day is not about aesthetics. Research consistently links regular aerobic and resistance training with improved executive function, faster cognitive processing, and reduced cortisol levels. Walking 10,000 steps builds in movement throughout the day, which prevents the metabolic stagnation that comes from extended desk work. The step target is simple, trackable, and sustainable across travel schedules and deal cycles.

A day in the life of a high-agency investor

| Time block | Activity | Performance benefit |

|---|---|---|

| 5:30 to 7:00 AM | Movement, fasting window, mindfulness | Cortisol regulation, mental clarity |

| 7:00 to 9:00 AM | High-priority strategic work | Peak cognitive window utilized |

| 9:00 AM to 12:00 PM | Meetings, negotiations, decisions | Energy maintained, focus sharp |

| 12:00 to 1:00 PM | Light nutrition, walking | Sustained afternoon energy |

| 1:00 to 5:00 PM | Analysis, communication, review | Structured work within energy envelope |

| 5:00 to 7:00 PM | Social time, family, learning | Psychological recovery, relationship capital |

| 9:00 to 9:30 PM | Wind-down protocol | Sleep quality optimized |

Sleep management is non-negotiable. Chronic sleep restriction, even mild, impairs working memory, emotional regulation, and risk assessment. Investors who optimize their sleep architecture are protecting their most important asset: clear-headed judgment. Seven to nine hours is the target. Consistent sleep and wake times matter as much as duration.

Here are the core energy and health habits that high-agency investors prioritize:

- Set a fixed eating window and protect it even during travel

- Schedule physical activity as a non-negotiable appointment, not an afterthought

- Track your daily steps and treat 10,000 as a floor, not a goal

- Build a wind-down routine that protects sleep quality consistently

- Block time for mental health practices, whether that's meditation, journaling, or structured breathing

Pro Tip: Don't wait for a slow week to start an exercise habit. Design your executive fitness strategies to function during your busiest periods. If the routine only works when things are calm, it's not a system, it's a wish.

Building performance longevity strategies means designing for your most demanding weeks, not your easiest ones. That's the standard worth building toward.

Integrating growth: Personal development in the investor lifestyle

Here is where most high achievers underinvest, often because they mistake busyness for progress. Learning and personal growth are not things that happen when you have spare time. At the top level, they are structured habits with dedicated time blocks, the same way meetings and portfolio reviews are.

Longevity investors consistently cite weekly social and learning time as critical for sustained vitality. This is not soft advice. It reflects a hard reality: cognitive adaptability, the ability to update your mental models, challenge your assumptions, and integrate new information, is a performance variable. Investors who stop learning at a deep level start relying on pattern-matching that worked in a previous era.

Micro-learning is the practical vehicle for most executives. Thirty minutes of focused reading in a new domain, one structured conversation with someone who thinks differently than you, a weekly podcast block during physical activity. These compound. Over a year, the investor who does this consistently knows more, thinks more flexibly, and makes better cross-domain connections than one who passively absorbs industry news.

Reflection is equally important and equally neglected. A weekly review, even fifteen to twenty minutes, where you assess decisions made, assumptions tested, and patterns noticed, builds the metacognitive layer that distinguishes exceptional investors from merely skilled ones. You are not just accumulating experience. You are processing it deliberately.

Personal development habits that high-performing investors build in:

- Dedicated weekly learning blocks, scheduled and protected

- Monthly one-to-one conversations with people outside their industry

- Quarterly reflection on strategic assumptions and mental models

- Regular input from diverse perspectives through curated reading or curated networks

- Annual review of personal growth goals alongside financial ones

Pro Tip: Link your learning blocks to your physical activity whenever possible. Audiobooks and podcasts during walks or cardio sessions let you compound two high-value habits without adding time pressure to your schedule.

Following healthy lifestyle routines and building the edge to sustain your executive resilience long-term both depend on this integration between continuous growth and deliberate recovery. You cannot optimize what you don't reflect on.

Why most investor lifestyle advice fails (and what actually works)

Most of what gets published about the investor lifestyle treats finance, health, and growth as separate lanes. Optimize your portfolio here. Follow a workout plan there. Read books when you find the time. That compartmentalized view is where the advice fails, and where most ambitious men lose ground they don't realize they're losing.

The real engine of sustained high performance is integration. Your financial stability directly affects your sleep quality. Your sleep quality directly affects your decision-making. Your decision-making directly affects your returns and your relationships. Your relationships and your learning directly affect your strategic adaptability. These are not parallel tracks. They are one system.

What we consistently see among the men who maintain genuine edge into their late 50s and 60s is this: they don't optimize one variable in isolation. They build buffers across every dimension, financial liquidity, physical recovery, cognitive reserves, and social capital, and they protect those buffers with the same discipline they apply to risk management in their portfolios.

The uncomfortable truth is that most performance advice is designed for people who have time to implement it. Real investors don't have excess time. They have to make hard choices about what gets protected and what gets cut. The high-performance living guide that actually works for this group is built around non-negotiable minimums in each domain, not maximum optimization of any single one.

Daily integration beats compartmentalized excellence. A man who sleeps well, moves consistently, keeps his financial stress low, and learns something new every week will outperform a man who crushes one of those variables and neglects the rest. The compounding effect of integrated habits, even modest ones, is the most underestimated force in long-term investor performance.

Take your investor lifestyle to the next level

The systems described in this article work. But implementing them alone, while managing a demanding portfolio and a full life, is harder than it needs to be. The men who move fastest are the ones who combine personal discipline with professional-grade support and access to tools built specifically for their level of performance.

VIRIDOS is a premium Swedish men's performance brand designed for exactly this context. Built for founders, investors, and executives who refuse to trade long-term vitality for short-term output, VIRIDOS delivers science-based performance solutions in small-batch formulations developed with precision and purpose. Whether you're exploring the science behind VIRIDOS or ready to access the full suite of executive-level solutions, the VIRIDOS Membership gives you a structured, premium pathway to integrating the habits that actually drive sustained edge. Your next decade starts with the systems you build today.

Frequently asked questions

How much emergency savings should an investor have for optimal financial well-being?

Vanguard research shows that at least $2,000 in emergency savings is linked to a 21% higher level of financial well-being compared to having none, and the principle scales significantly for high-net-worth individuals who need ring-fenced liquidity separate from investment capital.

What daily health practices boost investor vitality and focus?

Structured practices including intermittent fasting, approximately one hour of daily physical activity, and a 10,000-steps daily baseline consistently appear in the routines of high-performing longevity investors as the core drivers of sustained energy and cognitive clarity.

Does financial stability really affect investor performance?

Automation and emergency savings reduce stress and decision fatigue directly, and automated savings lower emotional load during volatile periods, which protects the cognitive bandwidth needed for high-quality strategic decisions.

How do top investors fit personal growth into a busy schedule?

They schedule weekly social and learning blocks as fixed appointments, often combining them with physical activity, rather than treating personal development as something that happens in leftover time.